Insights from Insurance Company Adjusters

Insights from Insurance Company Adjusters: The Common Practice of Lowering Estimates and Findings

In the wake of devastating natural disasters, homeowners rely heavily on the insurance company to provide fair and accurate assessments of property damage.

In a bombshell testimony at a Senate Homeland Security Committee hearing on Tuesday, May 13, 2025, it was uncovered by adjusters who worked at a large insurance company that lowering estimates and altering findings to save the insurance company money is a standard business practice.

A Case Study on How Insurance Companies Willingly Lower the Estimated Damage of Their Clients

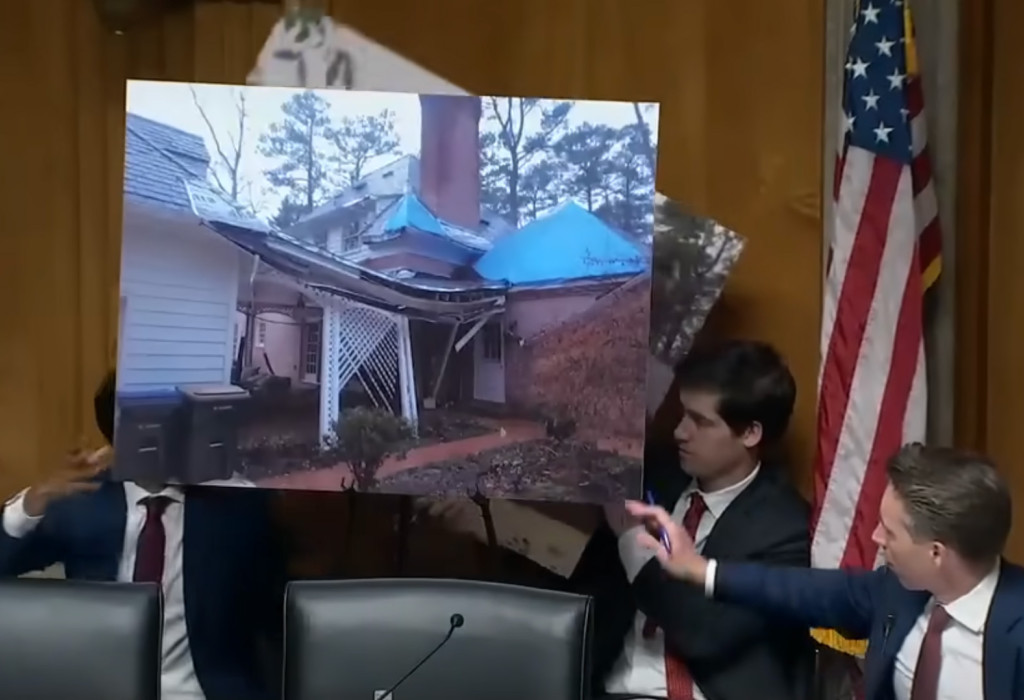

On September 27th, 2024, Hurricane Helen caused significant damage to a home in Georgia, resulting in extensive structural damage including a destroyed breezeway and severe roof damage, among other damages. The homeowner, who was insured by All-State, was relying on it to give them an honest assessment.

Mr. Schroeder, who worked for All-State, inspected the property for several hours and documented the damage as "extremely serious”. Accordingly, he prepared an estimate for a full replacement of all the damages, which the insurance company then told him to modify in order to lower the cost of the payout. Subsequently, Mr. Schroeder was then removed from the case; he expressed concerns that his removal was motivated by a preference of the insurance company to lower claim payouts rather than give the policyholder a fair evaluation of their damages.

Patterns of Pressure and Altered Assessments

Mr. Schroeder’s pressure to lower truthful estimates is not an isolated case! He acknowledged being frequently directed to reduce claim estimates and noted that refusal to comply often led to his removal of honestly estimated claims. This suggests a pattern of the insurance company consistently looking to pay the policyholder less than the true value of their damages.

Mr. Millikan who was assigned to replace Mr. Schroeder, confirmed that the damages to the policyholder’s property was in fact several hundred thousand dollars. Mr. Millikan’s estimate was also rejected.

In Mr. Millikan’s case, after reviewing extensive damage to a property that was supported by multiple reports, including one from an engineer as well as a public adjuster, he submitted an estimate to the insurance company recommending several hundred thousand dollars in payouts. Mr. Millikan’s estimate was rejected, and he was instructed to lower his estimate regardless of the truth. In a shocking testimony, he revealed that such directives to alter or delete factual findings, and occasionally include inaccurate information, were common practice. These alterations consistently resulted in reduced payouts for policyholders.

The Devastating Impact of Trusting the Insurance Company

Both adjusters agreed that the ultimate priority for the insurance company they worked for was to protect the bottom line of profits rather than paying out what was truly owed to the policyholders. This practice undermines the trust homeowners place in insurance providers and compromises the integrity of the claims process. Moreover, policyholders are generally not informed when initial adjuster findings are modified or rejected, limiting their ability to fully understand or contest the assessments of their claims.

Conclusion

The testimonies from seasoned adjusters confirm when insurance companies face large payouts, they often resort to modifying or outright rejecting honest findings behind the back of the policyholder.

Now, more than ever, it is important when property owners are facing significant damage, they retain an independent expert, like a public adjuster, to make sure they’re being treated fairly by the insurance company.

Video Summary

- Hurricane Helen hit Georgia on September 27th, 2024, causing significant damage to Miss Migal's home, including a massive tree fallen in front and extensive roof and breezeway damage.

- Miss Migal is an All-State policyholder; All State sent an adjuster approximately three weeks after the hurricane to inspect the damage.

- The first All State adjuster verbally agreed the damage was severe but later issued an assessment of only $46,000, far less than expected.

- Miss Migal hired an independent adjuster who estimated the damage at about $497,000.

- The initial All State adjuster, Mr. Schroeder, spent several hours inspecting the property and described the damage as extremely serious, the worst he saw on that deployment.

- Mr. Schroeder was instructed to downgrade the claim from a full to a partial replacement of the breezeway, and before completing his work, he was removed from the case, allegedly for taking too long.

- Mr. Schroeder believes he was removed because his thorough and high estimate was not aligned with All State's goal to lower payouts; he stated he was frequently told to reduce estimates and that refusal led to reassignment of claims.

- All State's priority, according to Mr. Schroeder, was protecting their bottom line rather than maximizing policyholder awards.

- Mr. Millikan, another All State field adjuster with extensive experience, was assigned to reinspect Miss Migal’s's home.

- Mr. Millikan confirmed the extensive damage and reviewed various reports, including an engineer’s and the public adjuster's.

- Mr. Millikan’s initial estimate recommended several hundred thousand dollars in payments, but All State rejected it and told him to lower the estimate.

- He was instructed to alter his estimate contrary to his own assessment, and although he documented these instructions, policyholders were never informed about these alterations.

- Mr. Millikan testified that he was frequently asked to alter or delete factual findings, sometimes even include false items, almost always resulting in lower estimates to policyholders.

- According to Mr. Millikan, All State’s ultimate goal is to protect their bottom line and maximize profits, using adjusters to achieve that end.

- Both adjusters testified that this practice of lowering estimates and altering findings is a pattern of All State’s practices, not just isolated to Miss Migal’s’s case.